|

|

Follow FACTUAL NEWS

on

|

|

|

|

||

|

|

||

| |||||||||

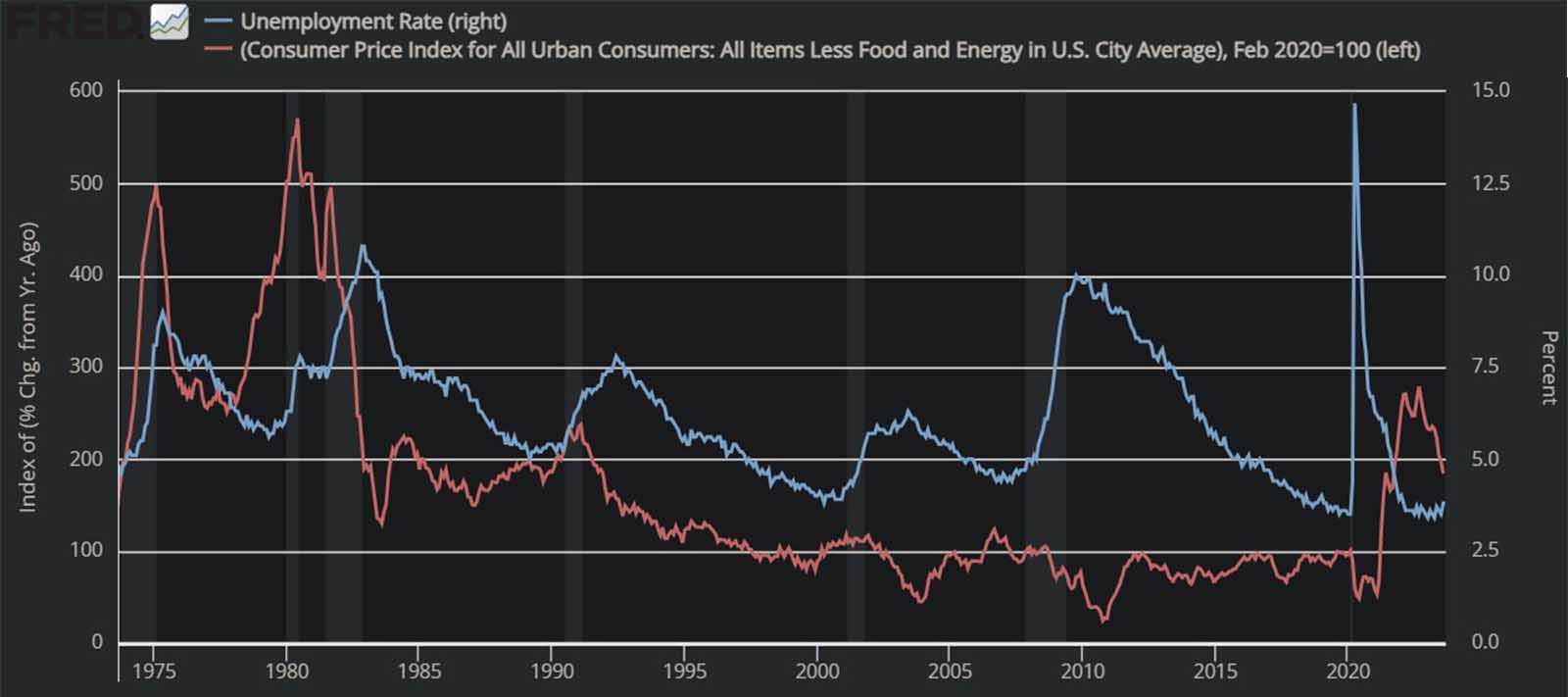

Raising Interest Rates did NOT Solving INFLATION !Sep 25, 2023: WASHINGTON (AP) — Last year inflation spiked to the highest level in four decades. Fortunately the FED's raising of

interest rates have made

no difference to Inflation.

Here are some reasons for the economy’s unexpected resilience and a look at whether it might endure:REPLENISHED SUPPLIES HAVE COOLED INFLATIONThe idea that defeating high inflation would require sharply higher

unemployment is based on a long-time economic model that may prove

ill-suited for the

post-pandemic episode. This inflationary episode, may end up more closely

resembling the one that occurred after World War II

The prices of nearly three-quarters of

goods and services have

declined as quantities have increased.

|

| Sen. Bernie Sanders recently introduced the Ending Corporate Greed Act. The act would impose a 95% tax rate on the excess profits of large corporations that earn more than $500 million a year. Excess profits are defined as profits that exceed the corporation’s average profit level from 2015 to 2019, adjusted for inflation. This excess profits tax will be imposed over and above the normal

corporate tax of 21%, but the two rates will be

coordinated so that the maximum combined tax rate will not exceed

75% of income for any year. This sounds radical (95% taxation!), but in fact it is not.

|

|

During the First and Second World Wars and the Korean War,

the US implemented a broad-based windfall profits tax.

During World War II, the tax rate reached as high as

95% , which ensured that companies could not profiteer off the war.

In addition, the US enacted a windfall profits tax on

oil and gas companies as recently as the mid-1980s.

The idea underlying these prior efforts was that companies should not earn

“windfall” profits, namely profits that result from external circumstances such

as wars or extraordinary rises in the price of certain commodities, and not from

their own efforts.

The current combination of the COVID-19 pandemic,

which raised the profits of companies like Amazon

to record levels, and the war in Ukraine, which did

the same to oil and gas companies, fully justifies reviving the

windfall profits tax.

The Sanders proposal is essentially identical with the Word War II version of

the tax, including:

| the reliance on a pre-war average, | |

| the 95% rate, and | |

| the limitation on the overall effective tax rate. |

Economists distinguish between

| normal returns to capital, which are subject to competition and therefore are relatively constrained, and | |

| rents or excess returns, which are not. |

Normal returns are a legitimate target of taxation, but the tax rate should not be too high because a high rate would deter companies from socially useful investments.

Excess returns, on the other hand, are those that are not subject to competition:

| quasi-monopoly status like Amazon or Google, or | |

| quasi-oligopoly status like ExxonMobil or Chevron, earns from their access to a unique resource and their domination of the market. |

Because excess returns are not subject to competition, taxing them at even

very high rates will not deter investments

because the remaining after-tax profit will still be a windfall.

Correctly distinguishing between

| normal profits taxed at the regular 21% rate and | |

| extraordinary profits taxed at 95%. |

The corporate tax is not primarily about

| revenue (it is less than 10 percent of total federal tax revenue) or | |||||

redistribution (it is unclear who bears the burden of the

|

The corporate tax is primarily about regulating large corporations by giving them

| tax incentives (for example, green-energy credits) and | |

| disincentives (like the proposed tax penalties for investing in Russia). |

The Sanders proposal is designed to regulate corporations that take advantage of

| the current inflationary wave, | |

| the pandemic, and | |

| the war in Ukraine |

to increase their profits way above their previous average profit.

Ideally, it would raise little revenue but induce a fall in prices, which would benefit everyone except corporate shareholders.

But if such a price decrease does not happen, the tax would raise significant

revenue (according to Sen. Sanders, an estimated $400

billion in one year from 30 of the largest corporate profiteers

alone).

These revenues could be used to subsidize working

families that suffer the effects of rising prices, and to

accelerate the shift to renewable energy so

that the economy is less at the mercy of the oil companies, domestic and

foreign.

SOURCE:

https://prospect.org/economy/time-to-tax-excessive-corporate-profits/

|