|

|

Follow FACTUAL NEWS

on

|

|

|

|

||

|

|

||

| |||||||||

Source

Baker & McKenzie - thankyou

We must, at least for now, prioritize on Locations with the cheapest production and stop all Exploration. WSJ March 2015: Wordwide 2010-2014 Banks earned $31 billion in fees financing Energy Cos :

The players: AlliedBernstein($35 billion), Citigroup, Goldman, UBS, Morgan Stanley but, for example Chase, BofA and Wells Fargo refused to buy them from Citi. In the past 10 years

Investment Banks made $1 trillion loans to

Energy Cos. most were sold to investors. They sold

much of the debt to loan Mutual Funds, 2011-2013

but investors withdrew $35 billion 2014 (according to

S&P

Capital IQ) International Oil and

Gas

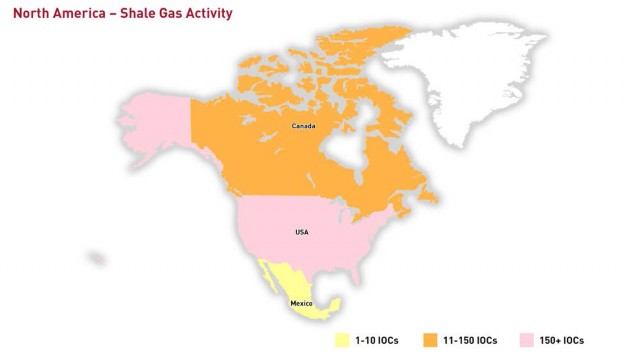

Companys ( IOCs ), with the majors leading the pack, have ventured outside the

US market to shale gas rich countries, to

try to be first on the ground and create a "shale

revolution". They have been encouraged in their

endeavours

by local governments, eager to emulate the US shale revolution.

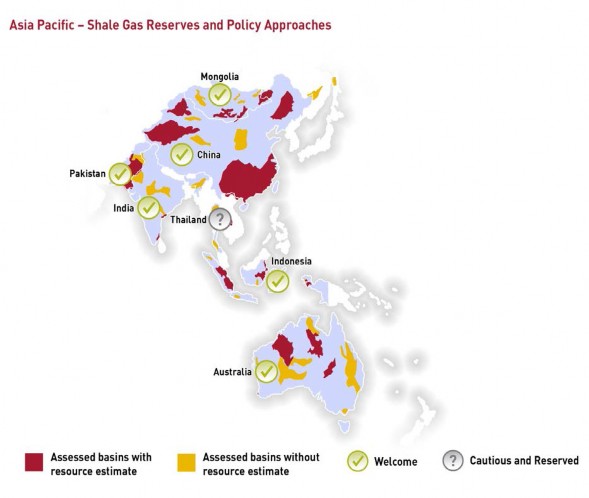

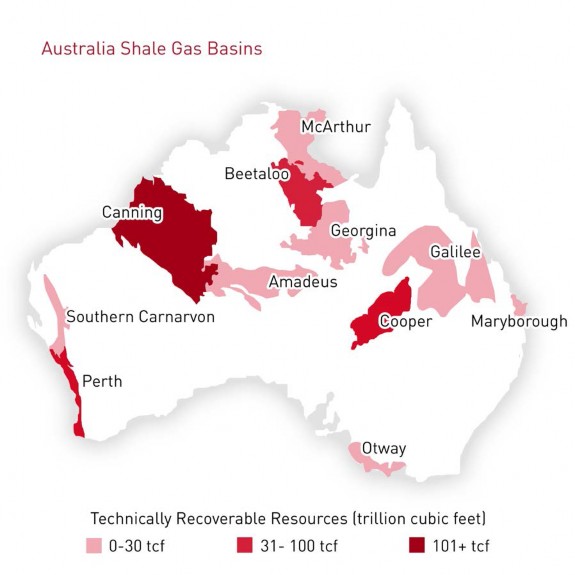

These "unexpected" obstacles are best exemplified in China, where the National Energy Administration halved its production goal for 2020 from 60 billion cubic metres ("bcm") to 30 bcm. Significant shale gas reserves in the US and accelerating shale gas production means that the US has a domestic surplus of natural gas that is outstripping current and projected domestic demand. This has led to falling imports of natural gas in the US, a redirection of natural gas destined for the US to other markets and opportunities for the export of US Liquid natural Gas ( LNG ). The impact on the global LNG market has been significant. For a facility to be economical, there must be a committed natural gas resource that is sufficient to enable the LNG facility to export gas for 20 years. Production from shale wells is not as consistent as from a conventional natural gas resource. The production curve is impacted by the volume of gas that is free (which is released very quickly) and the volume that is absorbed (which is released very slowly). If there is a proportion of free gas it can be released from day one of operations by fracking. However, there is a steep decline, typically between 70- 90% in the first year, as free gas is depleted, thereafter absorbed gas bleeds slowly through the low permeability reservoir from beyond the fracture to give a low production rate over the longer term. Therefore, multiple hydraulically fractured wells are required to produce shale gas in commercial volumes. This means that the capital cost of shale gas production extends throughout the production period as the field requires continuous drilling of exploration and appraisal wells. This also means that LNG sales contract commitments require greater flexibility. The realities of shale gas production certainly do not sit comfortably with traditional LNG models, which require enough proven reserves and a consistent production flow to allow the LNG facility to operate at or close to nameplate capacity. An isolated shale producing field is therefore unlikely to be able to underwrite the cost of a large-scale, greenfield onshore LNG facility. In Australia, significant unconventional gas developments centre on coal bed methane ("CBM") which collects in underground coal seams by bonding to coal particles. Some gas occurs in the natural fractures of the coal and some is dissolved in liquid in the coal seam, but the vast majority of methane comes from the coal's micropores. In order to release absorbed gasses from the coal surface, the process of "desorption", the pressure in the matrix of the coal needs to be reduced. This is achieved by removing formation water from the coal fractures, which causes the gasses to be released and diffuse through the network of fractures and cleats to the low pressure area around the well-bore in the same manner that they would in a conventional gas reservoir. Hydraulic fracturing or fracking is required to realise CBM. Therefore, the production of gas from CBM has raised many of the same environmental issues the shale gas industry is facing. However, technological advances supporting the development of CBM exploration and production on the east coast of Australia, combined with high Asian LNG prices owing to the high price of oil led to a number of Australian LNG projects being announced between 2009 and 2012. Among these projects are the Queensland Curtis LNG project ("QLNG"), the Gladstone LNG project ("GLNG") and the Australia Pacific LNG ("APLNG") project, which are currently being developed in Queensland, Australia. All three projects source CBM from the Surat Basin and the Bowen Basin, which are part of the Great Artesian Basin, one of the largest artesian groundwater basins in the world. These projects aim to export LNG to nearby Asian markets rather than sell to the less lucrative domestic market, with Australia expected to become the world's biggest exporter of unconventional gas in the short to medium term. However, the rapidly expanding shale gas industry in North America may impact this projection. Initially, these LNG projects adopted the integrated upstream model, with the owners of LNG plants largely holding interests in the vast CBM reserves that will supply the CBM to LNG plants. These projects were also each planning to build their own pipeline infrastructure. However, increased labour costs, operational pressures (including less production than expected) and a drop in oil prices have forced these projects to cooperate. The owners of GLNG and QLNG have now agreed to connect the two gas pipelines that will feed their projects. In addition, Origin Energy, the upstream operator of APLNG has agreed to sell 347 Bcf of gas to Santos, the owner of GLNG. A fourth Queensland natural gas export project, the Shell and PetroChina owned Arrow Energy, has also been proposed. However, Shell appears to be favouring a deal under which Arrow Energy's CBM would be processed by one of the existing CBM to LNG plants. Whether shale gas will be enough to justify and underpin LNG projects outside

of

North America and

Australia remains to be seen. However, one thing is clear: recent

developments, such as the abundance of natural gas in the

US, the ramping up of production in

Australia,

LNG project developments in

East Africa, the

Yamal

LNG project in

Russia and planned LNG projects in

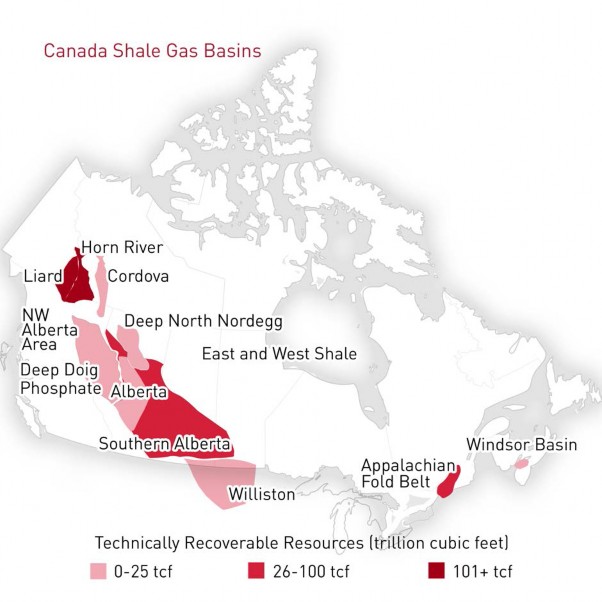

Canada, are changing the global energy market.

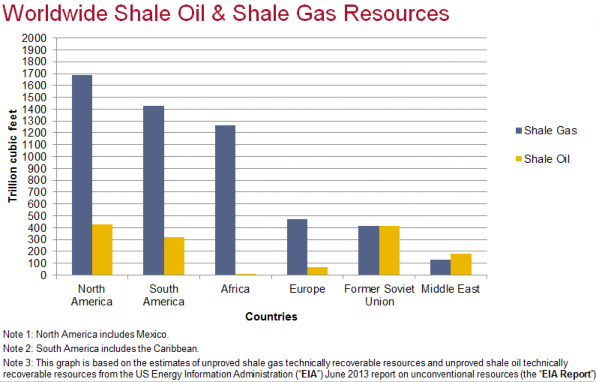

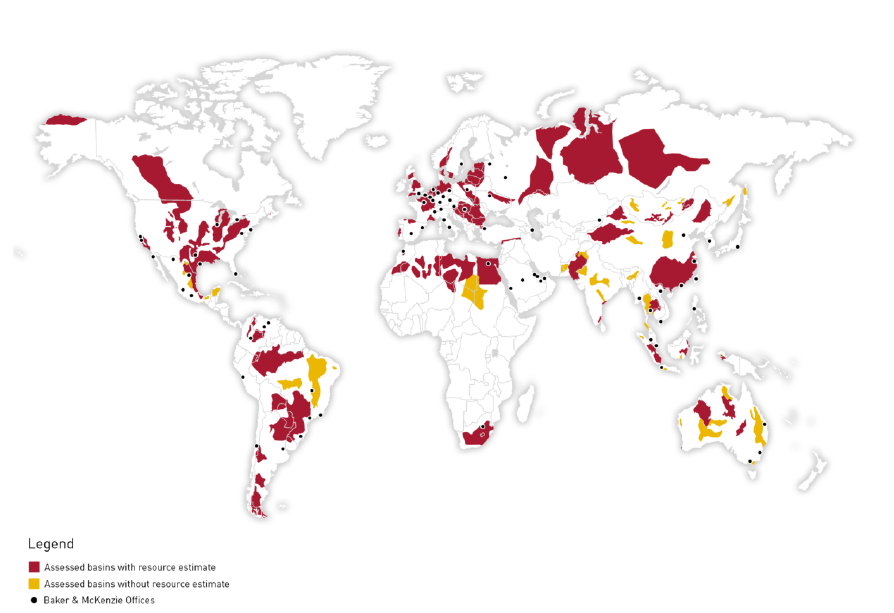

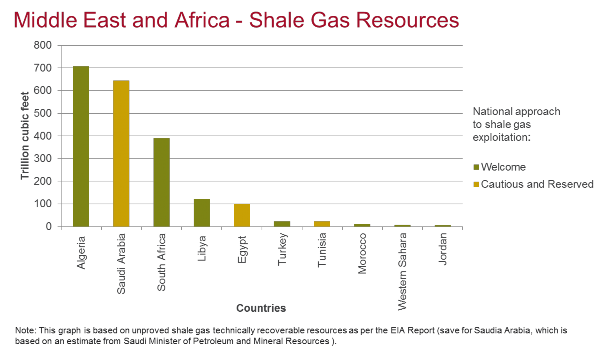

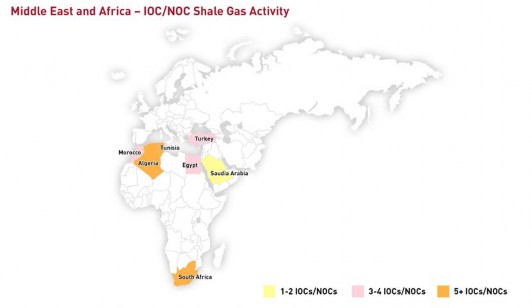

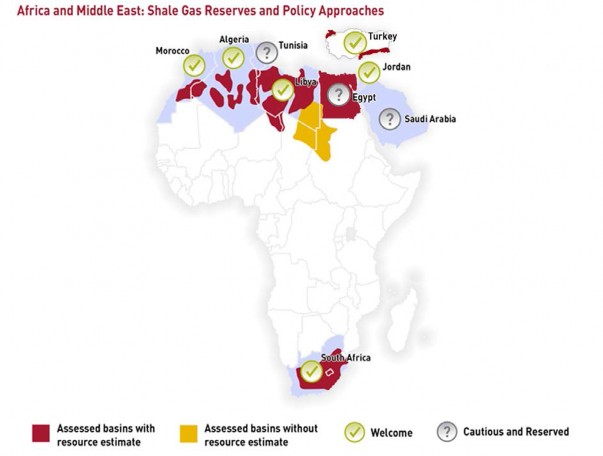

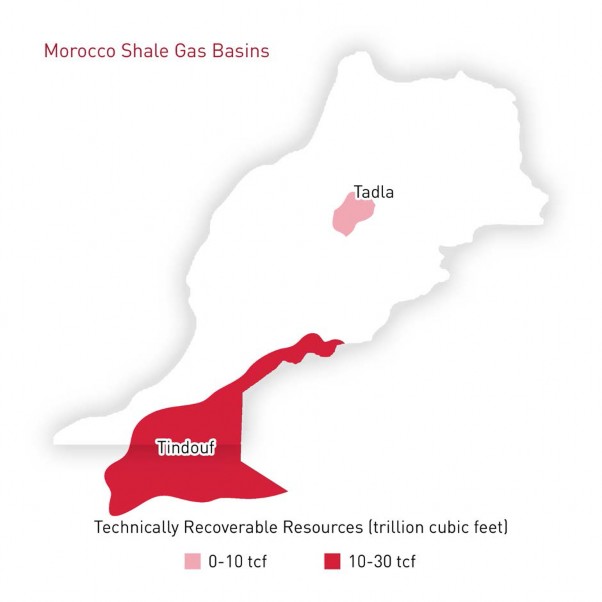

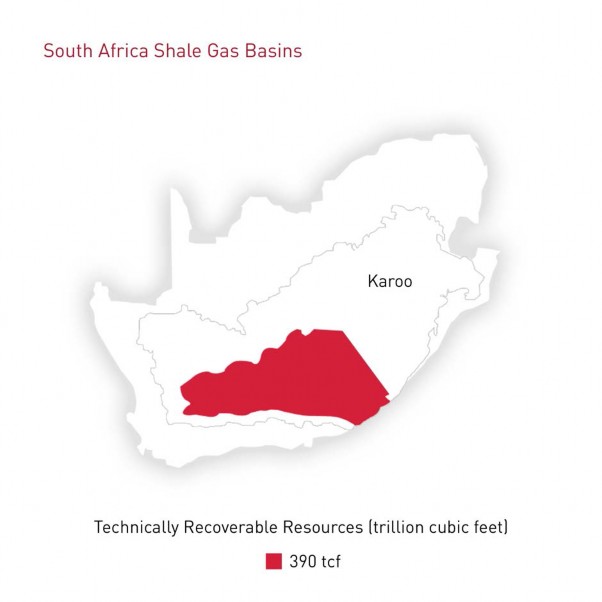

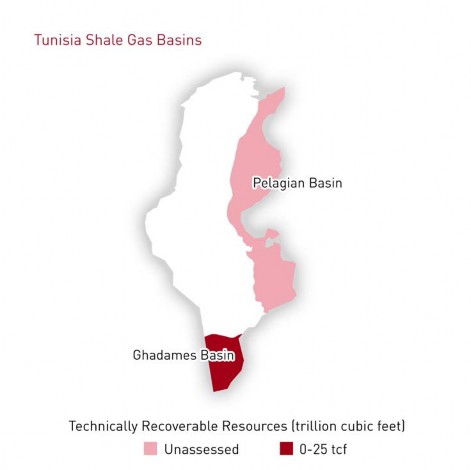

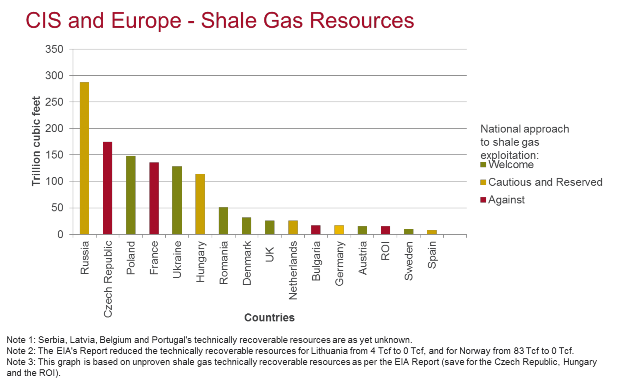

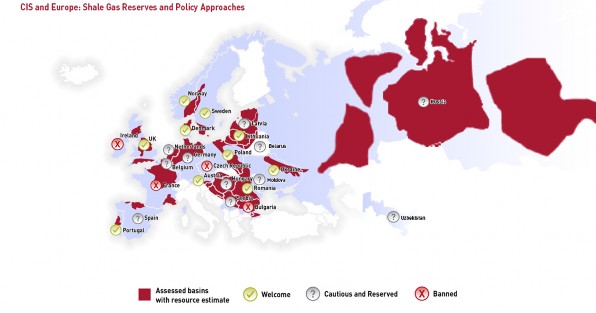

As displayed on the map below, in Africa and the Middle East, countries have either decided to welcome shale gas exploration or to take a cautious and reserved approach. There is currently no ban on, or outright opposition to, the exploration for shale gas in Africa and the Middle East regions. It is also worth noting that the region has significant shale oil reserves, notably in Libya, Algeria, Tunisia and Jordan and that governments and regulators in these jurisdictions have displayed a willingness to allow the exploration of these resources.

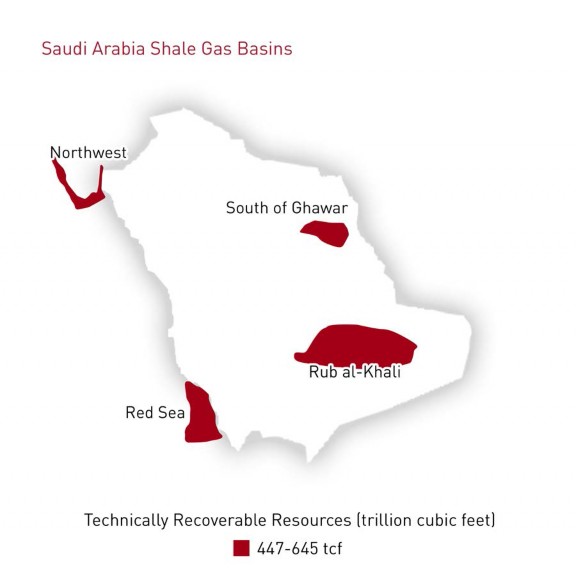

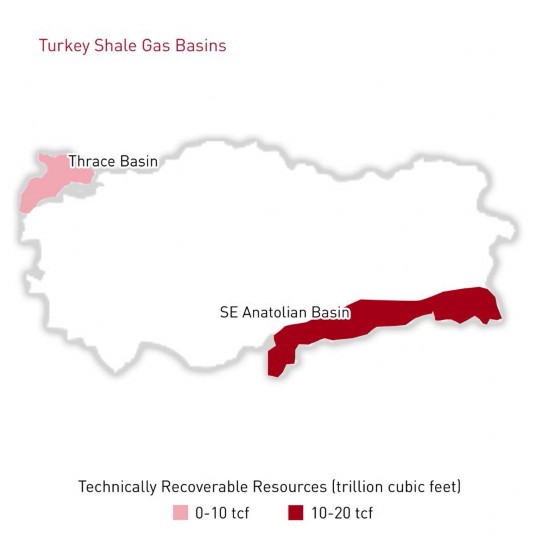

Studies have proved that,

in the Middle East, Jordan,

Turkey and Saudi Arabia

have technically recoverable shale gas resources at 7 tcf, 23 tcf and 645 tcf

respectively. In October 2013, Saudi Aramco announced that it would be ready to start producing its shale gas resources in the next few years. Saudi Aramco plans to use domestically produced shale gas to cater to the needs of its growing national energy consumption (with demand expected to double by 2030), thus freeing more oil for exports. In particular, there are plans to use shale gas as feedstock to fuel a proposed power plant in Jizan, which will be connected to a 400,000 barrels- per-day ("bpd") refinery. Saudi Aramco has already carried out exploratory and appraisal drilling in three prospective areas: the northwest, the south Ghawar and the Rub' al-Khali, where it has since been confirmed that Russia's Lukoil will begin drilling with Saudi Aramco for unconventional gas in early 2015. However, developing its shale gas resources is not Saudi Arabia's priority, and efforts are currently centred on its vast conventional hydrocarbon reserves. Saudi Arabia is shelving its planned crude output capacity extension from 15 million bpd to 12 million bpd and the re-direction of a third of Qatar's gas exports from the US to China. However, things must be kept in perspective. The US is only beginning the process of converting its LNG import terminals into LNG export terminals, with plans to cap the number of LNG export terminals to non-Free Trade Area countries and to impose export quotas. Such caps and quotas aim to retain sufficient natural gas to fuel the re-birth of petrochemical and manufacturing industries in the US (i.e. lower fuel costs enable companies to price products more cheaply and hence to be more competitive on the international markets). The time needed to convert an LNG import terminal into an LNG export terminal (approximately three to four years), the planned caps on the number of such terminals, quotas on the amount of gas available for export and the time needed to re-direct oil production to Asian markets effectively mean that rising production in the US does not constitute an immediate threat to the Gulf's oil exports and petrochemical industry. In the medium term, provided economic growth keeps its pace in the Asian markets, Asia's hunger for energy is set to continue increasing, providing a stable customer base for the Middle East's oil exports. This, coupled with a rising domestic energy consumption (growing 8% to 10% annually) in the Gulf and the natural gas/oil price sensitivity of shale gas projects (i.e. shale gas projects are not economically feasible if natural gas/oil prices decline below a certain point) means that the Gulf oil and gas industries can still feel confident about the future. However, this does not mean that Gulf countries should ignore some of their latent problems such as subsidised domestic oil and gas prices and heavy reliance on t he oil and gas industry as the driver of economic growth. Gulf countries would be wise to take a long term view and continue on their path of industry diversification and consider cutting domestic subsidies for oil and gas.

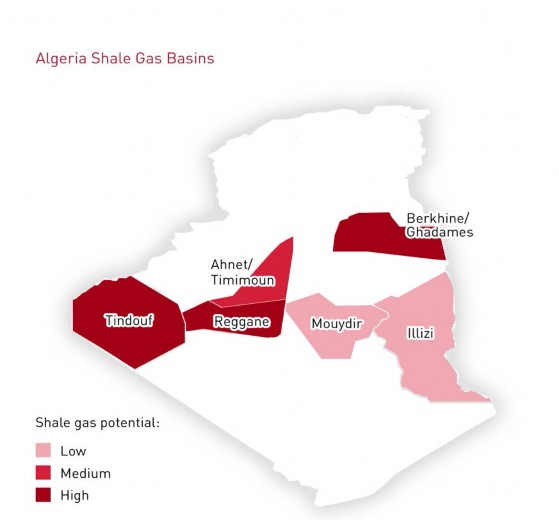

Sonatrach

SpA

("Sonatrach"),

the country's NOC,

owns 80% of hydrocarbon production in Algeria under

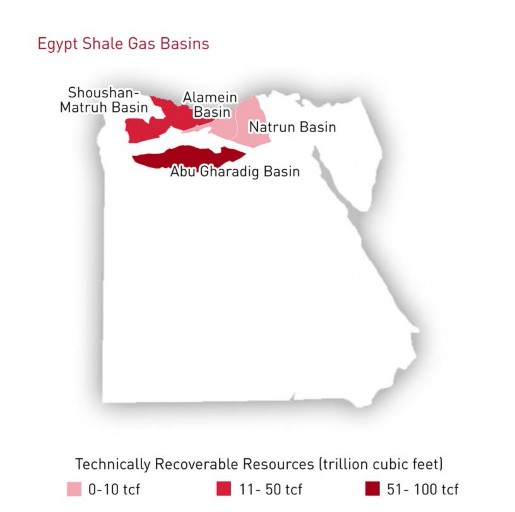

a legal majority stake requirement, with the remaining 20% owned by IOCs. Egypt shale gas exploration: EGPC,GANOPE, EGAS, Shell and Apache Corporation (Khalda Petroleum Company -- a joint venture between Apache Corporation, EGPC and Sinopec)

|

|